A version of this article originally appeared in Forbes.

The SaaS market has transformed rapidly over the last several years, and operators need new growth strategies to thrive in a new normal. To better understand these shifts, I spoke with revenue operations expert Eliya Elon about key opportunities and challenges facing today’s SaaS companies. Here are some of our thoughts on how to build resilient, high-growth businesses in times of uncertainty.

If you’ve started a career in B2B SaaS in the last two decades, you’ve lived almost exclusively in a growth-at-all-costs world.

Things have now changed: as interest rates rise, boards increasingly expect B2B SaaS businesses to operate with a capital efficiency that we’ve typically associated with non-high-growth industries.

We predict that this is not a passing trend. As efficient growth becomes the new normal, ops leaders and their counterparts in sales, marketing, and customer success will be charged with making it happen.

In the coming years, we’ll observe how companies transition through emerging case studies. For now, let’s discuss potential strategies that companies might adopt:

Strategy #1: Strengthening their Ideal Customer Profile (ICP)

Strategy #2: Shifting to market-oriented forecasting instead of capacity planning

Both strategies are challenging. Enhancing ICP demands better coordination among sales, marketing, and customer success teams, while market-oriented forecasting necessitates advanced data handling. When combined, though, these approaches enable companies to operate much more effectively in markets limited by growth rather than capacity.

Real-world examples of ICP focus and ICP neglect

Selling to a customer who isn’t the best fit for your company strains resources in several ways:

- Marketing uses more budget to persuade them.

- Sales invest more time justifying your product’s value.

- Customer success dedicates extra effort to assist with implementation.

These ill-fitting customers are also more prone to churn, as they don’t fully benefit from your product’s value. This churn forces marketing to seek even more customers, sometimes beyond the ICP—all of this perpetuates the cycle.

Neglecting ICP discipline has long-term consequences while, by contrast, companies with a strong ICP focus within their go-to-market (GTM) strategy often experience efficient growth. Let’s look at examples of both.

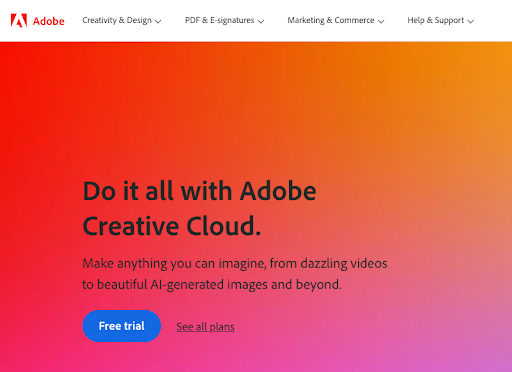

Adobe: How ICP focus leads to operational excellence

Adobe began making the switch to subscription-based billing in 2012, and in the last five years has posted an average operating margin of 33% with extraordinary consistency. ICP focus is core to that success, and you can see it reflected across Adobe’s homepage.

Although Adobe sells dozens of products to a wide array of end users, they bucket their GTM (certainly marketing, as far as we can tell) into three areas:

- Creativity and design (Adobe Creative Cloud), purchased by creative teams and is a high-growth product that takes up most of the homepage

- PDF and e-signatures, purchased by general and administrative teams and is a necessary utility

- Marketing and commerce (digital analytics and associated products), purchased by analytics teams and has a strong base of large enterprise usage (less of a growth business, but > $1 billion in annual revenue)

By aligning its marketing, product, sales, and support strategies with specific ICPs, Adobe enhances its operational efficiency. This allows each business unit to cater effectively to its designated customer group.

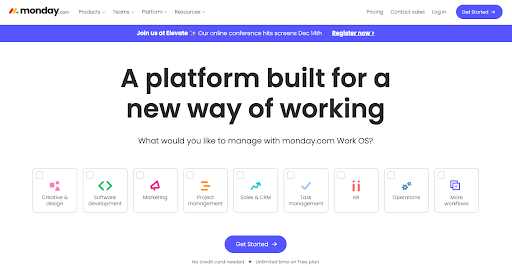

Monday.com: The flip side of ICP focus

For a counterexample, let’s examine Monday.com’s homepage. There we see a list of teams (like creative and design, software development, marketing, HR, and more) and a mix of use cases (such as CRM, project management, and task management). The question naturally arises: Who is their main audience? It seems to be everyone.

While this broad appeal might work for marketing, targeting a more specific audience that aligns well with the product could potentially lead to greater external efficiency. A narrower focus might reduce customer acquisition costs and lower the resources required to support and retain these customers. Of course, it’s important to note that Monday.com has been exceptionally successful—this isn’t intended to be a critique but rather an observation. Without their internal data, this is just a hypothesis pointing out the potential benefits of a targeted ICP, and we’re big fans of the efficient model that Monday.com has built.

Moving beyond capacity-based forecasting

In a growth-at-all-costs world, capacity is everything.

In forecasting, pipeline and net-new revenue was a function of marketers and sales reps hired. This is especially true in a supply-constrained hiring market like the one we saw through 2020-2022, where it was often quite difficult to hire enough GTM staff to meet growth targets.

But in focusing on capacity-based forecasting, we end up treating every employee and territory equally—ignoring the market opportunity presented to those new hires, which will of course vary widely depending on the patch they’re assigned to work.

Efficiency is about pushing the limits of production to maximal output. If we’re attempting to maximize revenue from a given team’s size constraint, we need to develop a more nuanced understanding of what drives actual sales productivity.

A new class of modern Chief Revenue Officers (CROs) is meeting this challenge by bringing a much more data-intensive view on measuring productivity. One example is replacing capacity-based forecasting with forecast modeling that incorporates macroeconomic signals: a bottom-up snapshot of a business’s current actual addressable market in a given territory or segment.

For example, if you know a target account just signed a multiyear deal with a competitor, you wouldn’t count that opportunity as part of a given sales rep’s addressable book of business.

This requires much more data sophistication than a simple capacity-modeling spreadsheet, but the payoff is that your revenue model maps closer to market reality in the field.

The bottom line: By combining ICP discipline with more sophisticated forecasting, you can put your GTM organization in a much better place in terms of operational efficiency.

But what’s required to get there? There’s currently no playbook to pull off the shelf to implement these strategies.

Strengthening partnerships between ops and data organizations

Operators and their friends on data teams are already close collaborators at most B2B SaaS businesses, and the efficient growth imperative only puts further positive pressure on these relationships.

ICP discipline requires developing a single definition of ICP across marketing, sales, and customer success datasets, and implementing that in data tooling used across teams. That in itself is a big lift!

But without that basic ICP observability, there’s no way for GTM organizations to reasonably experiment with or point themselves toward a desired ICP. Think about it: if you wanted to subtly shift your company’s definition of a “best fit” customer or get various functions (marketing, sales, CS) to stay disciplined around an existing definition, how would you do it?

It’d likely require a lot of coordination, even if you had datasets perfectly dialed in and well distributed in the company.

The same goes for moving to market-based forecasting: entirely new datasets must be brought into data warehouses, and new form factors for forecasting (beyond the spreadsheet-based capacity model) must be devised to validate market-based forecasts.

Our work is cut out for us! Efficient growth is the key to unlocking the true potential of the SaaS model, and the most advanced operators recognize that the pace of transition will be governed by the quality of your ops and data team collaboration.

Revenue operations expert Eliya Elon co-authored this article. Eliya was previously a senior go-to-market leader at Rapid7 and is an advisor at data-driven companies like Salto and Hightouch.